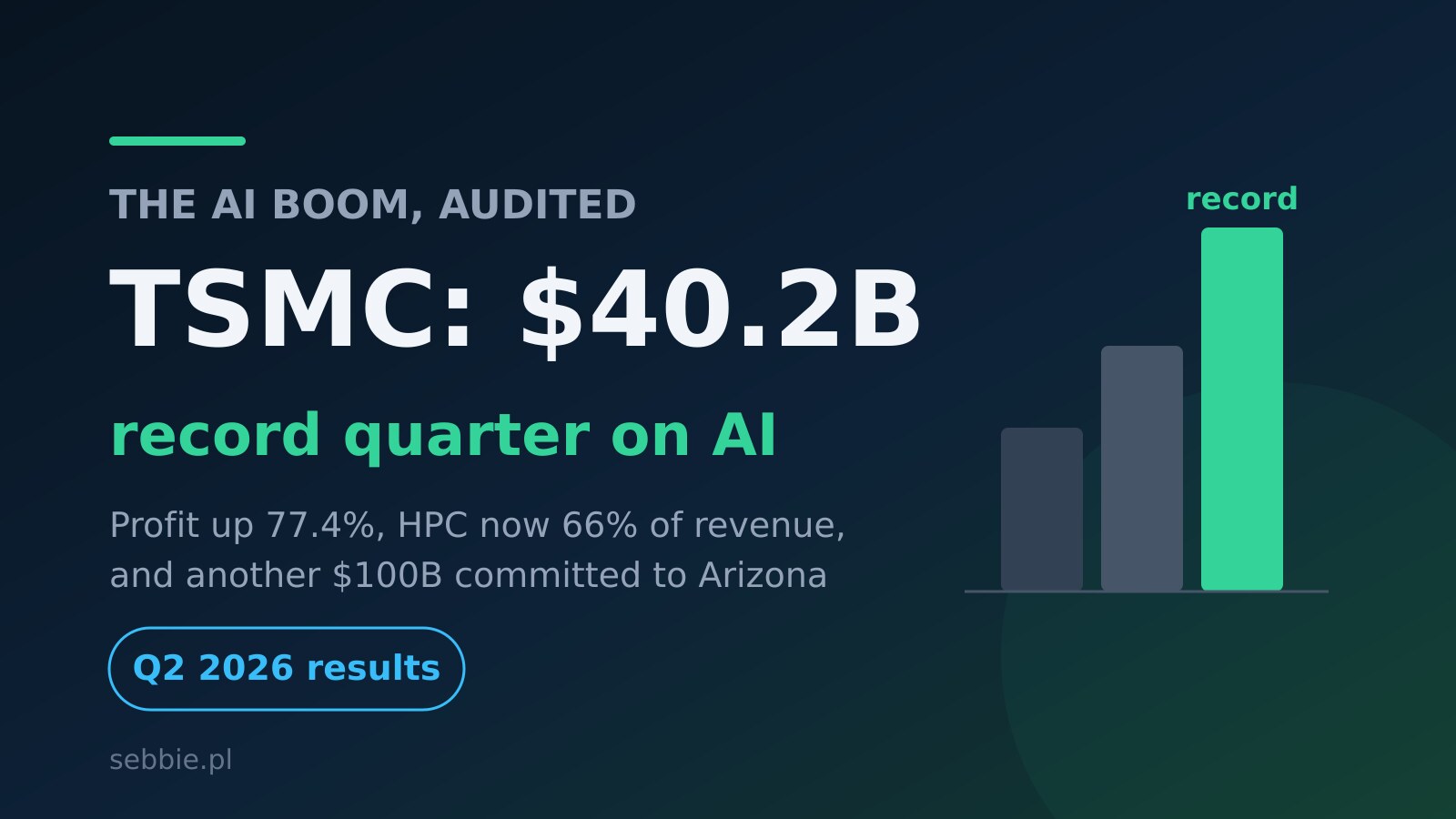

Every few months the AI industry argues about whether we are in a bubble, and every few months one company quietly publishes the numbers that settle the argument - at least for that quarter. On July 16, 2026, TSMC reported its Q2 results, and they are, by any historical standard for a manufacturing business, absurd: 40.2 billion dollars in revenue, up 36% year over year, a net profit that jumped 77.4% to a record NT$706.56 billion, and a gross margin of 67.7% - a number that would make a software company nod in approval, achieved by a company that etches silicon. The TSMC record quarter matters well beyond Taiwan, because TSMC is the one company through which essentially the entire AI boom physically passes. When you want to know if AI demand is real, you do not ask the labs. You ask the foundry.

The TSMC record quarter in numbers

Let me lay out the headline figures, because each one tells a slightly different story:

- Revenue: 40.2 billion dollars, up 36% year over year - a new quarterly record.

- Net profit: NT$706.56 billion, up 77.4% - also a record, and growing twice as fast as revenue.

- Gross margin: 67.7%, above the company's own guidance ceiling.

- High-performance computing - the category that includes AI chips - generated 66% of revenue, growing 20% quarter over quarter.

- The 2-nanometer node (N2) contributed its first meaningful commercial revenue: 3% of wafer sales.

- Full-year 2026 revenue growth guidance raised to slightly above 40%.

- An additional 100 billion dollars of investment in Arizona announced, bringing total committed US spending to 265 billion dollars.

Profit growing at more than twice the pace of revenue is the detail I would underline. It means TSMC is not just selling more wafers - it is selling them at ever better prices, because the things customers want (leading-edge nodes, advanced packaging) are exactly the things nobody else can supply at scale. That is what a monopoly on the frontier looks like in an income statement.

Two-thirds of TSMC is now an AI company

The revenue mix shift is the structural story. High-performance computing at 66% of revenue means the phone business - which built TSMC and defined it for two decades - is now a side hustle. Nvidia's GPUs, the custom accelerators from Google, Amazon and the labs, the CPUs that feed them: that is the center of gravity now, and it grew another 20% quarter over quarter at a company already this size.

This is what makes TSMC's earnings the best single thermometer for the AI buildout. Model labs can hype, cloud providers can bundle, but foundry revenue is brutally honest: chips were either ordered and paid for, or they were not. A 36% revenue jump with raised full-year guidance says the hyperscalers' capex promises - the hundreds of billions announced across 2025 and 2026 - are converting into actual silicon orders, not sitting in press releases. Demand is, in the CEO's own recurring phrase, very strong, and specifically from AI customers.

The N2 node reaching 3% of wafer revenue deserves its own note. Every previous node transition took quarters to reach commercial meaningfulness; 2nm hitting 3% in what is effectively its first real quarter signals that the leading-edge customers - Apple first, AI accelerator designers right behind - are paying up immediately. When compute is the bottleneck for an entire industry, nobody waits for the price curve to mature. And with reports that Anthropic and others are exploring custom inference silicon on 2nm-class processes, the queue for that node only gets longer.

The 265 billion dollar geography lesson

Alongside the earnings, CEO C.C. Wei announced another 100 billion dollars for Arizona, bringing TSMC's total committed US investment to 265 billion dollars. It is worth pausing on that number: it is among the largest industrial investments any company has made in any country, ever - and it is happening under sustained pressure from Washington to de-risk the fact that the world's most important manufacturing capability sits an hour's flight from mainland China.

I keep coming back to a theme on this blog: AI is bifurcating along geopolitical lines - models, regulation and now atoms. The same week that Apple Intelligence entered China running on Alibaba's Qwen because Western models cannot cross that border, TSMC committed another hundred billion to building leading-edge capacity inside the United States because Washington no longer accepts the concentration risk. Software divides along jurisdictions; now the fabs are following. The bifurcated AI world is being poured in concrete, at nine-figure sums per building.

What this means if you build with AI

It is tempting to file semiconductor earnings under "investor news" and move on, but a few practical implications reach all the way down to those of us who just use these systems:

- Compute stays scarce into 2027. Guidance above 40% growth means TSMC's leading-edge capacity is effectively sold out; demand is growing faster than fabs can physically be built. Token prices for frontier models have room to fall only as fast as efficiency gains outpace this scarcity - do not count on dramatic cuts.

- The efficiency wave has a tailwind. Scarce, expensive compute is exactly why the industry is investing in 1-bit compression, doom-loop fixes and small-model reliability - the themes I covered with Bonsai 27B and Antidoom. Every wasted token now has a visible price attached.

- Custom silicon is rational, not vanity. With margins like 67.7% flowing to the foundry and Nvidia stacking its own margin on top, every large lab doing the math on custom inference chips reaches the same conclusion. Expect more such projects, and expect them all to queue at the same two or three fabs.

- The bubble question has a boring answer. Whatever happens to AI startup valuations, the physical layer is running at record utilization with raised guidance. If this is a bubble, it is one where the pick-and-shovel seller has two-thirds of its business in picks and cannot make them fast enough.

The caveats a record quarter deserves

Before anyone reads this as "nothing can go wrong", the honest counterweights. First, foundry revenue is a lagging indicator of decisions made quarters ago - chips ordered in 2025 optimism land in 2026 results, so a demand crack would show up here last, not first. Second, customer concentration cuts both ways: when two-thirds of revenue rides on one category, largely driven by a handful of hyperscalers and one dominant GPU vendor, a single capex pause at a single company moves the whole number. Third, the margin story has a currency asterisk - a strong Taiwan dollar has been eating into margins all year, and 67.7% came despite that headwind, which is impressive but also a reminder that macro can move these numbers independently of AI demand. And finally, the Arizona buildout, for all its scale, will take years to produce leading-edge wafers in volume; the concentration risk it is meant to hedge remains fully live today. None of this changes the quarter's verdict. It just defines what would have to break for the verdict to change - and what I will be watching for in October's report.

Summary: the boom, audited

TSMC's Q2 2026 is the AI boom expressed in the only language that cannot exaggerate: recognized revenue. A record 40.2 billion dollar quarter, profit up 77.4%, two-thirds of the business now high-performance computing, a brand-new 2nm node already selling, guidance raised above 40% for the year, and another 100 billion dollars committed to American soil for geopolitical insurance. Strip away every demo, every launch event and every open letter, and this is what remains: the world's most important factory says AI demand is real, growing, and physically constrained. For better or worse, that is the ground truth the rest of the industry - and this blog - gets built on.

Sources: Yahoo Finance, Investing.com.